New Deal for Buy One, Get One Free Flights on Southwest Through February 2026

One of the most popular promotions offered by Southwest Airlines is back for a limited time. You can earn ‘buy one, get one free’ flights via the Southwest Companion Pass and 30,000 Rapid Rewards bonus points right now. This post covers details of this special offer, the timeframe to take advantage, pros & cons, and everything you need to know.

Let’s cut to the chase with specifics. Starting today (February 4, 2025) through March 31 2025, Southwest Rapid Rewards Plus, Premier, and Priority Consumer Credit Cards from Chase are giving new credit cardholders the opportunity to earn the coveted Companion Pass from Southwest, plus 30,000 Rapid Rewards bonus points—after spending $4,000 within the first 3 months from account opening.

With this promotional Southwest Companion Pass, new credit cardmembers can bring a travel partner along for free on as many flights as they’d like through February 28, 2026 (not including taxes and fees from $5.60 one-way). This is an unlimited BOGO flight deal, and the Companion Pass applies to both paid and award flights booked with points. Here’s our referral link for the special Southwest Companion Pass deal. Before clicking that, we strongly recommend reading on for the downsides to this deal and superior alternatives.

Normally, you can obtain the Southwest Companion Pass by flying 100 one-way qualifying flights or earning 135,000 qualifying points in a calendar year. The full, non-promotional version of the SWA Companion Pass is then valid through the end of the next calendar year.

Even as a frequently-flying blogger, I’ve never hit the requirements the “honest” way of notching 100 flights. I don’t even think I’ve flown half that number in our best year. That’s not to say the alternative of credit card spend is dishonest–since SWA is not aimed at business travelers, I’m guessing it’s how more than 90% of travelers qualify for the Southwest Companion Pass.

It’s worth emphasizing that the promotional Southwest Companion Pass through the limited-time welcome offer that runs through March 31, 2025 is only valid through February 28, 2026. To maintain your Companion Pass status after that, you’ll need to qualify through these methods of qualifying flights, points earned, or rinse-and-repeat on this deal (which seems to be offered around this time every year).

The non-promotional Southwest Companion Pass is good for the full calendar year after the year you earn it.

This means that a Companion Pass earned in February 2025 expires on December 31, 2026 because you earned it this year. A Companion Pass earned in December 2025 would still expire on December 31, 2026.

That’s almost a full year of extra use simply by timing the spending requirements “correctly.” You want to earn it as close to the start of the calendar year as possible. We’ve earned the full version of the Southwest Companion Pass a few times, and with savvy spending, hit our goal by the first week in January and kept it until December 31 of the following year. That’s almost two full years of the Companion Pass, as opposed to one under this promo.

To earn the Companion Pass, what we’ve always done is open two Southwest Chase credit cards, one personal card and one business card.

Before I lose half of you, something as pedestrian as selling on eBay or Facebook Marketplace qualifies you for a business card. You do NOT need to register as an LLC, do any fancy corporate tax filings, or submit an executive summary to Chase to qualify for a business credit card. You just need to apply for the Southwest business credit card. That’s literally it.

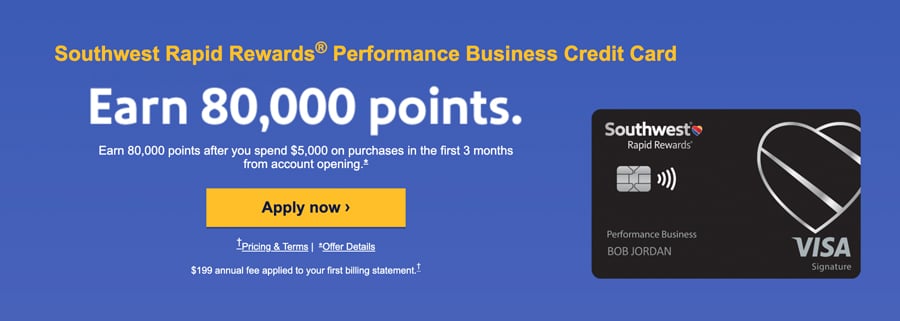

Chase Bank offers the Southwest Performance Business credit card with a sign-up bonus of 80,000 points after you spend $5,000 on purchases in the first 3 months from account opening. (You can earn these bonuses via our referral link–just toggle over to the black business cards at the top.)

Along with that, get any of the three personal SWA credit cards but NOT with the promotional Companion Pass. We recommend the bottom tier, as it has the lowest annual fee and this card is going to be largely redundant to the Southwest Performance Business card. With any of those, you earn 50,000 points after you spend $1,000 on purchases in the first 3 months from account opening.

In tandem, you will earn over 135,000 Rapid Rewards points once you meet the minimum spend. (Bonus points of 130,000 plus spending of at least $6,000.) It should be pretty easy to hit that $6k spending requirement…just take a trip to Walt Disney World!

Of course, there are several reasons why the promotional Southwest Companion Pass might be the more attractive offer. Perhaps you have a Walt Disney World Annual Pass this year that you want to get mileage out of, but will take next year off. Maybe the $4k minimum spend is attainable, but not the $6.

You might be comfortable applying for 1 credit card, but not 2 from the perspective of how it’ll impact your credit score. As you’re likely aware, how you manage your open lines of credit (including credit cards) can affect multiple factors that determine credit scores, including your payment history, credit utilization rate, average age of accounts, and credit mix. Just like lotto tickets aren’t the best retirement plan, it’s probably not a good idea to get financial advice from a dude who blogs about Disney.

From our perspective, going the 2 credit card route is much better, but that’s for us. Only you know your circumstances and which approach is the right fit for you. There’s a reason the promotional Companion Pass is so popular whenever it’s offered, and we’ve heard from readers in the past who felt like the business card approach was too daunting (again, you don’t need a traditional business).

Another important thing to keep in mind here is Chase’s 5/24 rule. With this, you won’t be able to get most Chase cards if you’ve opened five credit card accounts across all banks in the past 24 months. Qualifying for the Southwest Companion Pass via credit cards and signup bonuses knocks out 1 of your 5. (Not 2, as business cards aren’t reported to the personal credit bureaus.)

If you’ve read the post to this point, that’s probably not a concern for you. The Chase 5/24 rule is aimed at hardcore hackers (or, I guess, serial spenders), who are not the target audience of this post. Still, if you’re considering getting into the wonderful world of travel hacking and are more inclined to fly internationally and on other airlines, you should give serious consideration to whether you want to burn a card on Southwest Airlines.

If you’re a couple or family primarily traveling to Walt Disney World or Disneyland, the Southwest Companion Pass is pretty much a no-brainer. There are few signup bonuses with as much potential as this one–the ‘value ceiling’ on the Southwest Companion Pass is incredibly high! When paired with an Annual Pass and room-only discounts (or better yet, Disney Vacation Club), the Companion Pass is a fantastic tool for inexpensive trips. It’s also a dangerous one, as it provides you an excuse for regular long weekend getaways to Walt Disney World.

We’re not kidding. Getting the Southwest Companion Pass in our newlywed years was one of the best decisions we’ve ever made. It resulted in us taking many more trips to Walt Disney World and Disneyland than we would’ve without the Companion Pass. In a roundabout way, it also unleashed all of my rambling thoughts on the internet! (So “sorry” or “you’re welcome” for that, depending on your perspective.)

Not to end this on a sappy note or anything, but we’re firm believers in the value of travel to expand horizons, learn about the world and yourself. The Southwest Companion Pass is a great conduit for all of that. It also allowed us to see the United States and have many memorable experiences together that shaped our relationship and who we are. And to be clear, this blog is not actually funded by a generous grant from Chase Bank, Visa, The Walt Disney Company, or Southwest Airlines (…yet?). We’re just really passionate about travel and see the value it has had in our lives. We know many people are averse to credit cards, but you can really leverage signup bonuses like this (and plenty of others) to fund travel that otherwise might be out of reach. All without paying a single cent in interest, so long as you’re responsible.

Planning a Walt Disney World trip? Learn about hotels on our Walt Disney World Hotels Reviews page. For where to eat, read our Walt Disney World Restaurant Reviews. To save money on tickets or determine which type to buy, read our Tips for Saving Money on Walt Disney World Tickets post. Our What to Pack for Disney Trips post takes a unique look at clever items to take. For what to do and when to do it, our Walt Disney World Ride Guides will help. For comprehensive advice, the best place to start is our Walt Disney World Trip Planning Guide for everything you need to know!

YOUR THOUGHTS

Have you ever had the Southwest Companion Pass? Did you earn it the ‘honest’ way or take advantage of credit card hacking to obtain it? Are you a fan of SWA or do you prefer other low cost or legacy carriers? Will you try for Southwest’s Companion Pass this year? Going the 2 credit card route, or the simpler promotional Companion Pass that’s valid through February 2026? Do you agree or disagree with our advice? Any questions we can help you answer? Hearing your feedback–even when you disagree with us–is both interesting to us and helpful to other readers, so please share your thoughts below in the comments!

I followed your links to the credit cards, but it seems the only personal cards you can apply for right now are with the Companion Pass promotion. Do we need to wait until this deal has passed to utilize the two card hack? Alternatively, what if I use the Companion Pass promotion and get the pass through February 2026, but get the business card later in the year and start earning points, getting to the required 135,000 points just after that Companion Pass expires. Is that possible?

Well, I earned a SW Companion pass once… In February of 2020.

If anyone is new to the credit card churn hobby, please read other blogs with more details. You must wait 24 months from your last bonus before you apply again for the same credit card, to receive a new bonus on the same credit card. Lots of blogs out there on how to churn travel credit cards. Also the Chase 5 cards every 24 months is an important rule to follow.

I’ve been doing the two-card method for nearly a decade, and it was great while it lasted, but Chase has significantly tightened up approvals within the last year. I used to be able to reliably get approved for both Southwest cards and a couple Inks within a few months, but that’s a lot harder now.

Another decent option is the temporary Companion Pass they offer every few months. For example the recent version was:

“Register for the promotion and purchase a qualifying Southwest® flight (one round trip or two one-way qualifying flights), starting Sept. 3 through Sept. 5, 2024.

Travel by Nov. 20, 2024; and

Designate a Companion to fly for free1 with them between Jan. 6, 2025, and March 6, 2025.”

Do that promo a couple times a year and you can get some solid value out of it without ever needing to open a card.

Tom, I’m not a financial advisor (nor did I stay at a Holiday Inn Express last night) but I know that applying to multiple credit cards within a short period of time can cause a decent hit on your credit score. The credit score also gets dinged when you close an account. That is going to be more significant for some than for others — for example, if your score is in the “fair” or “good” range (high enough to get approved, at least) you might be knocked down a tier. And if you’re thinking about taking out a mortgage, HELOC, or other loan in the months ahead you may want to hold off on this style of travel hacking (the score will eventually rebound, but no guarantee on timing).

Not to mention that for many, having extra incentive to spend (besides the minimum spend, there’s the psychological impact of having more “runway” to purchase beyond your means) can be tempting at best and dangerous at worst. All this additional travel you’re doing with the points and pass might feel like “free money” but it may involve costs for hotels, entertainment, food, cars/Ubers, etc. that you wouldn’t have been spending otherwise. (If you already have a bunch of trips lined up where you and a companion were planning to take Southwest at regular price, that’s a different story).

I’m not trying to be a Debbie Downer — I love travel hacks and I’ve used similar approaches on applying to other airline rewards cards (like United, when they offered both a boatload of miles and reimbursement of a Global Entry application). If you are financially disciplined/responsible, have decent (or better) credit, and/or aren’t planning to apply for any major loans in the next several months, then by all means, hack away. Just thought this “disclaimer” should be noted.

Also, you stated this: “You might be comfortable applying for 2 credit cards, but not 1.” Freudian slip?

Excellent points, all around.

I definitely wouldn’t do this right before applying for a mortgage, but if you’re in a position where a temporary hit to your credit score won’t have any impact, travel hacking a great option. I would hope people aren’t getting personalized financial advice from random Disney bloggers, but you never know–so that’s a worthwhile disclaimer.

And thanks for the heads up about the typo.

Tom, per the “financial advice” you’ve earned enough credibility and saved your readers enough money with various tips/hacks/strategies/advice (much of it related to saving money!) over the years that you might have more sway over your readers than you realize!

Plus, you give us peeks into your life — personal things like your daughter’s given name being Megatron and what the back of her head looks like. You’re not just a random Disney blogger — you’re FAMILY.

“The Chase 5/24 rule is aimed at hardcore hackers (or, I guess, serial spenders), who are not the target audience of this post.” Those of us in the hobby prefer the term “churners” LOL

Hard disagree.

Churners could be people who cycle through credit cards for rewards, or people who make their own butter. Not very cool.

Hackers make you sound tech-savvy and highly intelligent, like Nicolas Cage trying to steal the Declaration of Independence. Very cool.

Those who join a streaming service for a brief time, for one show, then quit, are those who “churn”, in the terminology of that industry. That is somewhat similar to this behavior of moving in and out of credit cards. I guess I’d call it “gaming” the system a bit, but since Disney expressly encourages phone-based gaming in a number of respects (like signing up for Virtual Queues…) I’d say it may reasonable to try something like this to mitigate the costs of a Disney vacation.

But please please people, don’t do this unless you clearly have the means to pay off the ENTIRE credit balance EVERY time. Carrying a balance into future months can clobber you with interest charges, especially once your teaser rate expires. You don’t want your own finances to resemble certain 2008 banks, right?

“But please please people, don’t do this unless you clearly have the means to pay off the ENTIRE credit balance EVERY time. Carrying a balance into future months can clobber you with interest charges, especially once your teaser rate expires. You don’t want your own finances to resemble certain 2008 banks, right?”

This is obviously good advice, and I agree wholeheartedly. We’ve obtained tens of thousands of dollars worth of credit card benefits over the years and have never paid a cent of interest. (Annual fees are an entirely different story–we pay a ton of those, but they’re always mitigated by benefits.)

Generally speaking, I wouldn’t worry about this when it comes to hardcore hackers or churners, though. The hobby takes a tremendous amount of savvy, effort and discipline, the kind of which that almost certainly translates to financial discipline as well. People are not putting all of the work into gaming the system, only to have their efforts be undermined by paying interest.

Reddit @ r/churning would disagree, but hackers does sound better. You are certainly correct about folks that routinely sign-up for credit cards to get the subs. They not only know what the 5/24 rule is, they also know to never carry a balance as sky high interest rates more than eats up and subscription bonuses you get. If you really want to juice your credit score you pay the balance before it is due to keep your credit utilization low, which increases your score. My P2 was worried that having lots of cards open would decrease her score, but in reality, it increases the amount of credit available to you and if you keep your credit utilization low your score will improve the more cards (unless it is so high that no improvement is possible). But you do have to watch your application velocity. It is a fun hobby that has allowed us to take trips and stay places we would probably not do if paying. Only been in the hobby for a few years but have already taken advantage of $1,000s of what I label in my spreadsheet tracker as “Free Stuff”.

If we were to go the two-card route, would that be repeatable once the Companion Pass expires?

It is repeatable, but not immediately.

During our heyday of Southwest Companion Passes, we’d rotate–so Sarah would apply for the cards in her name to qualify for ~2 years, and then I’d apply for the next round. This is the easy workaround for a couple.